Fixed Income Research & Macro Strategy (FIRMS) 31 January 2019

- The ongoing trade war between the US and China undoubtedly contributed to the slowdown in Chinese GDP growth to a nine-year low of 6.4% yoy in Q4 and (re)ignited concerns that China is in trouble. However, this slowdown needs to be put in context.

- For starters, this gradual downturn in Chinese GDP growth is probably a reasonably accurate reflection of the economy’s underlying path, in our view, despite repeated claims that official data are “massaged” and “smoothed”.

- Second, the slowdown from 6.8% yoy in Q1 2018 has been rather modest and if anything less acute than the slowdown in the rest of the world from about 3.0% yoy to 2.5% yoy.

- Moreover blaming weaker Chinese (and global) economic growth on Chinese domestic policies ignores the many factors exogenous to China – including tighter global monetary policy – which have contributed to slower growth in the world at large.

- Finally, the ongoing slowdown in Chinese growth partly reflects a conscious, long-term decision to sacrifice some headline “low quality” and unsustainable growth for slower but “higher quality” and more sustainable growth, in our view.

- This far from painless structural rebalancing of the economy will likely see Chinese growth slow further medium-term and weigh on other economies and corporates but also offer opportunities to regional economies willing and able to pick up the slack.

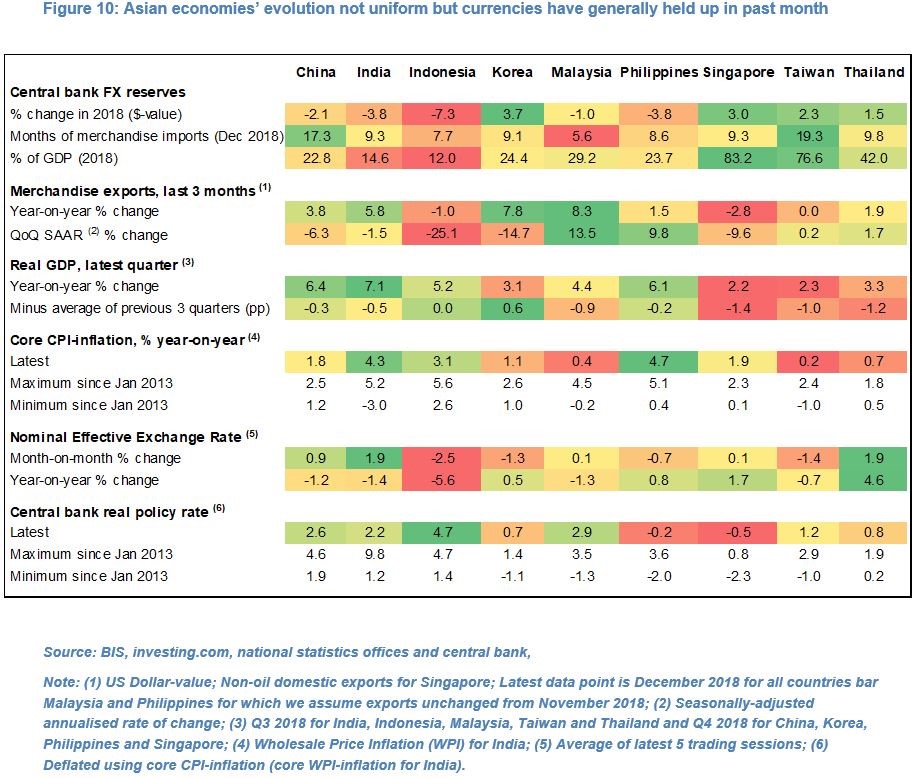

- Non-Japan Asian (NJA) economic and trade growth may slow in coming in quarters, partly as a result of weaker Chinese imports and global economic growth and higher domestic (and global) interest rates. However, on the whole NJA economies have so far shown a degree of resilience, at least relative to other emerging market economies and to history.

- Going forward, the sharp fall in global energy prices in Q4 and stimulative growth-policies in NJA should partly mitigate endogenous and exogenous headwinds, particularly for large net importers of oil and gas. This should in turn reduce any pressure on these economies’ currencies or at least fade their central banks’ incentives to allow or generate a weakening of their currencies – a theme we will explore in greater detail in our next FIRMS report

For the full research note, a free 30-day trail is available.

4X Global Research is a London-based consultancy providing institutional and corporate clients with focused, actionable, independent and connected research on Emerging and G20 fixed income and FX markets and economies.

4X Global Research has a strong forecasting track record, rooted in both a qualitative and quantitative analysis of data, trends, policy decisions and global events. Its conflict-free and unbundled research services aim to give investors a unique edge in their investment decisions. Its exclusive subscription-based reports and consultancy services form the basis of a long-term strategic partnership with its clients.

Psychedelic chartist extraordinaire. Have your shades ready.

Philosophy: “Don’t be a Dick for a tick”

Read how Ryan got into trading here

Philosophy: “Don’t be a Dick for a tick”

Read how Ryan got into trading here

Latest posts by Ryan Littlestone (see all)

- The last NFP competition of 2022 - December 1, 2022

- Will this month’s US NFP be a horror show? - October 4, 2022

- US NFP competition – Do you think there’s going to be a turn in the US jobs market? - August 31, 2022