Fixed Income Research & Macro Strategy (FIRMS) from 4X Global

- Media and analyst reports focussing on the scope for further US Dollar weakness and Emerging Market currency outperformance have continued to proliferate in the past month.

- The consensus view is still seemingly that a Democratic administration will fuel large US twin deficits and expectations of higher domestics inflation while Fed will keep rates on hold, eroding the value of Dollar assets. At the same time a pick-up in global confidence, economic growth and risk appetite will benefit EM and commodity currencies.

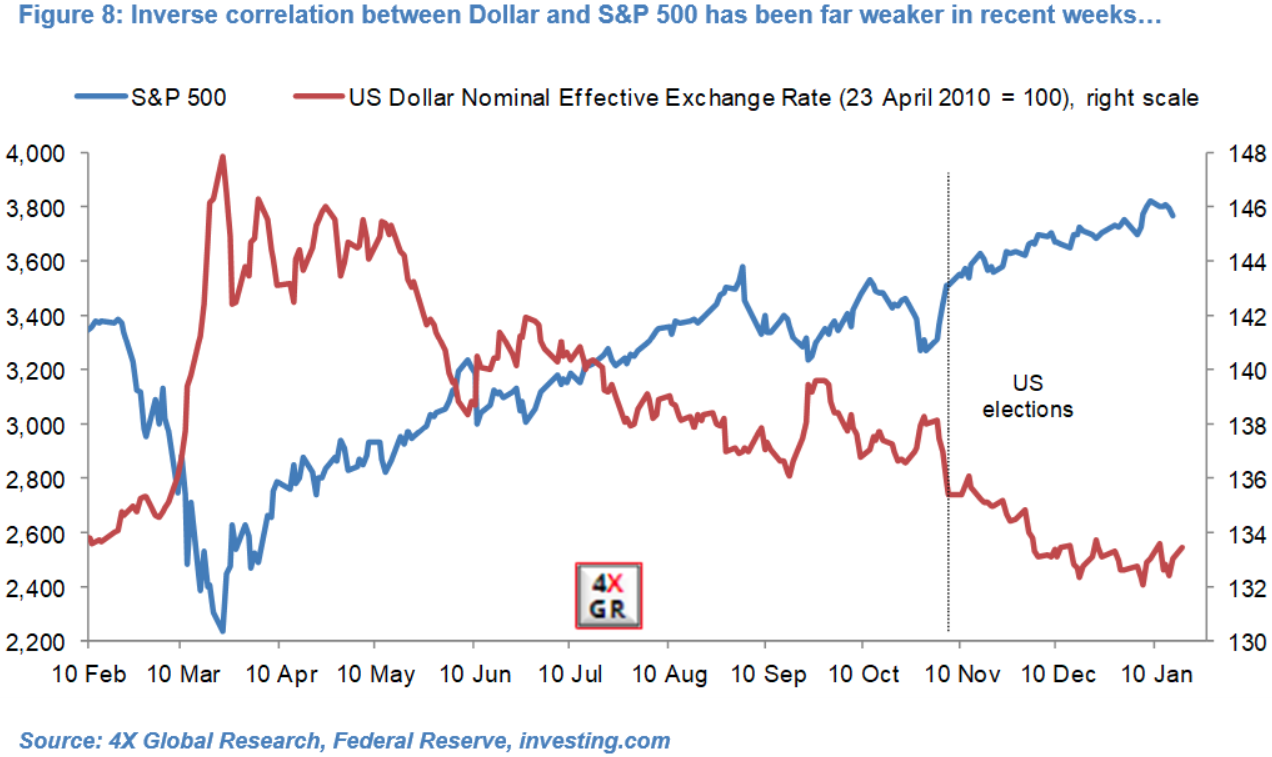

- While the “safe-haven” Dollar weakened sharply and EM currencies outperformed in the wake of the US elections on 3rd November recent facts tell a different story. Since 10th December the Dollar Nominal Effective Exchange Rate (NEER) and GDP-weighted baskets of developed and EM currencies have been broadly flat according to our calculations.

- Central European and Latin American currencies, which outperformed in November, have underperformed in past five weeks. Emerging Asian currencies, including the Chinese Renminbi, have done little since 10th December pointing to still active central bank FX management. This price action has broadly tallied with our near-term view that EM currencies will be “prone to sharp sell-offs (even if short-lived)”.

- Our analysis suggests that the steepness of the US Treasury yield curve rather than inter-country yield spreads matters more for the Dollar.

- However, we think central banks and sovereign wealth funds’ diversification out of Dollars into other reserve currencies, including Euro, Sterling, and Canadian, Australian and Kiwi Dollars, between May and early December was the main driver of Dollar depreciation.

- Dollar NEER’s stability since 10th despite a further 2.7% gain in the S&P 500 suggests this diversification process has stalled, which we think is partly due to stretched valuations. At the same time price action points to a rotation out of the Euro into Sterling.

- We stick with our view that Dollar depreciation may not resume for another couple of months and will in any case not be as broad based as in November/early-December with markets paying greater attention to domestic factors, including valuations.

For the full research note, a free 30-day trial is available.

4X Global Research is a London-based consultancy providing institutional and corporate clients with focused, actionable, independent and connected research on Emerging and G20 fixed income and FX markets and economies.

4X Global Research has a strong forecasting track record, rooted in both a qualitative and quantitative analysis of data, trends, policy decisions and global events. Its conflict-free and unbundled research services aim to give investors a unique edge in their investment decisions. Its exclusive subscription-based reports and consultancy services form the basis of a long-term strategic partnership with its clients.

Psychedelic chartist extraordinaire. Have your shades ready.

Philosophy: “Don’t be a Dick for a tick”

Read how Ryan got into trading here

Philosophy: “Don’t be a Dick for a tick”

Read how Ryan got into trading here

Latest posts by Ryan Littlestone (see all)

- The last NFP competition of 2022 - December 1, 2022

- Will this month’s US NFP be a horror show? - October 4, 2022

- US NFP competition – Do you think there’s going to be a turn in the US jobs market? - August 31, 2022